Prieur du Plessis of Plexus Asset Management is on the same page as me. However, his basis for an upcoming rally has more to do with market data trends. The first is the advance/decline spread which tracks the difference between advancing and declining issues and is widely used to measure the breadth of a stock market advance or decline. The chart below shows that the spread between declining and advancing issues on the NYSE has been moving in the right direction (for bulls) since the November lows and is actually again in positive territory.

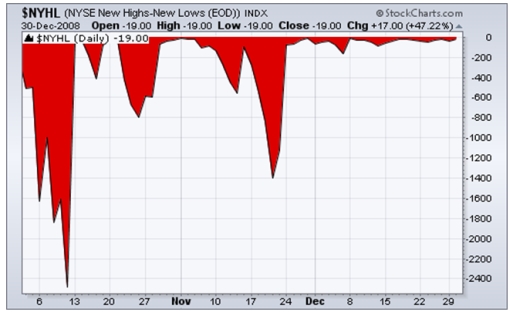

Net new highs are calculated by subtracting the number of new 52-week lows from the number of new 52-week highs. The panic day of October 10 marked an “internal bottom” when 92.6% of the stocks on the NYSE broke to new lows (whereas a “price bottom” was recorded on November 20). Net new highs have since improved markedly, but new lows are still in excess of new highs.

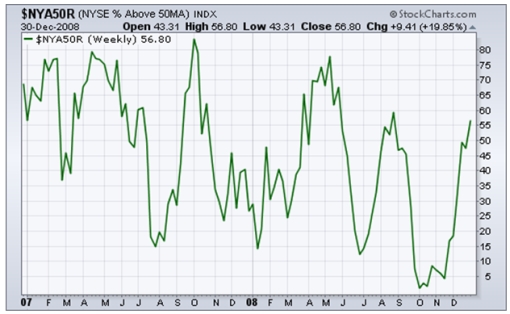

The number of NYSE stocks trading above their respective 50-day moving averages has increased to 56.8% from almost zero in October. In order to be bullish about the secondary trend, one would expect the majority of stocks to be above the 50-day line. For a primary uptrend to manifest itself, the bulk of the index constituents also need to trade above their 200-day averages. This is a slow indicator, but the number at the moment is still a non-existent 8.0%.

None of us will ever forget 2008, a year of extraordinary headlines. Bill Gates is no longer Microsoft boss. The US is no longer the world's financial model. The world's biggest investment banks have vanished. This columnist is still not rich and famous. (Just thought I'd slip that in.)

It was the year in which many of us heard things that we never thought we'd hear.

For example, I was stunned in September to hear this REAL quote from a US Treasury Department spokeswoman, explaining how the US$700 billion (HK$5.46 trillion) number was chosen for the Wall Street bailout: "It's not based on any particular data point - we just wanted to choose a really large number."

So THAT'S how they do it. The world's most powerful financial experts sit in a big room and make up a number.

"Er, how about 70?"

"Why 70?"

"It's my IQ."

"Mine, too. No, wait, hang on. Maybe it should be bigger."

"Okay, how about 700?"

"Let's make it WAY bigger, in case we get a percentage."

"Okay, 700 BILLION."

"Yeah, that'll do. Let's adjourn for a drink. Saving the world financial system is thirsty work!"

Or perhaps the most amazing quote of the year came from US Treasury Secretary Henry Paulson who proposed a law saying: "Decisions by the secretary may not be reviewed by any court of law or administrative agency."

I wonder how THAT conversation went?

He must have phoned George W Bush. Paulson: "Hey, Dubya? I need a favor. Can you pass legislation putting me totally above the law so I can do anything I like?"

Bush: "Sorta like God, you mean?"

Paulson: "Yeah, that's about right."

Bush: "Sure! Anything for my ole buddy."

And it's not just international politics, either. In our personal lives, we all heard people saying things that we couldn't imagine them saying a year ago, thanks to a range of unexpected news events - from the contaminated melamine milk scandal, to the rise of Australia's Putonghua- speaking Prime Minister Kevin Rudd.

Here are the top 10 most unexpected utterances of 2008:

1. Cleaner to investment banker: "Let's meet for coffee. Don't worry, I'll pay."

2. Parent to child: "Put down that milk. If you're thirsty, go drink Coke."

3. Parent to child: "See that black guy on TV? He's just been elected president of the United States of America."

4. Newscaster to audience: "A US court found OJ Simpson guilty as charged, and sentenced him to a long jail term."

5. Adult to adult: "You invested in the world's largest banks? No wonder you lost your money. You should have opted for something less dodgy, like a teenage dotcom start-up."

6. Chinese citizen to protester: "Sure you can trust the government. Just ask a Tibetan."

7. Contestant to quizmaster: "What's the capital of Iceland? Er, 10 dollars?"

8. Visiting Caucasian leader to Chinese leader: "Let's talk in Putonghua. And, no, I won't need the interpreter."

9. Parent to child: "No, darling, Captain Jack Sparrow is not a Somali."

10. Richard Dawkins, who made a fortune with his anti-religious best-selling book: "Thank God I'm an atheist."

# Why is there a trial in China on the tainted milk incident, but no trial on the many school buildings that collapsed during the recent quakes (amidst much older buildings left still standing among the rubble) killing thousands of children?

# Why is Santa a perfect anagram for Satan, why hasn't more been written about this?

# Why is it that resource rich countries always do much worse economically and in development compared to countries that have little or no natural resource?

# Why did I just pay RM176 for 2 nice pieces of prime OZ ribeye weighing 800gm (pp RM88), but 10 minutes later paid RM85 for medium sized new fan by KOK? One is to be enjoyed over twenty minutes while the other required dozens of parts to be assembled and probably will keep me cool for at least a couple of years.

# Why are we always highlighting our differences in Malaysia, when we should be highlighting our shared identity, destiny and social responsibility?

# Why is religion almost always responsible for most wars and skirmishes? Where is the peace and love that are so fundamental to all religions? Where is the forgiveness, where is the other cheek, where is the thou shalt not kill ... I think if God were to return today, he would say "THIS IS NOT WHAT I MEANT, YOU IDIOTS!!!"

# Why is there still so much persecution and bias against a person's race or lifestyle? Where is the peace and love, where is the love for all mankind, who is your neighbour? We may abhor the "acts" but we must love the person first. ... ... I think if God were to return today, he would say "THIS IS NOT WHAT I MEANT, YOU IDIOTS!!!"

I have 3 children under 7 years. My eldest goes to a US based homeschooling class of 3-5 students per class for 3 hours a day.

1) Responsibility Before the class starts, the students have to sweep the floor, wipe the table and chairs, arrange them, and wash the toilet.

2) Thought process Instead of learning mainly ABCs, they start with character building and phonics. They are encouraged to write of their activities and feelings as their school work.

Hone presentation skills-show n tell in class develops their self-confidence and public speaking from young.

3) Buy their own toys I do not buy any toys that my children want. There is a reward chart at home for good behaviour, duties, obedience. Upon achievement of a set of "stars" they get to go to a park, stay over at friend's house, eat sushi, etc. That is the adult world that they will eventually face. If the toy costs RM20, they need to earn it by washing the car, help the maid in cleaning and other house chores @ RM1 each. Upon earning their money then they can buy their toy (sometimes with a little subsidy from us) and they actually take care of their hard-earned toys better. We are amazed that they are actually so very eager to do their chores everyday once you place a carrot in front of them.

Some say that will create calculative kids, but you mean the parents are able to be calculative with their bosses but the kids can't? We also teach them to tithe their income.

4) Creativity Limit the TV and PC. They learn to make figurines and vehicles from old boxes and paper and sticks, coz mommy and daddy are not buying them the entire Toys r us.

A good ref. is Dare to Discipline by Dr James Dobson.

Whatever it is, children need and yearn for boundaries. We as parents can teach them by setting goals relevant to their age, teach them to be independent from young.

Yuppie parents esp love to spoil the kids with the best PS2, and other material stuff to compensate for lack of communication and time.

My own youngest sis with straight As love to hop from job to job for a mere RM150-200 increment. I lost count of the no. of jobs. They are not interested in learning any skills, unfortunately.

Maybe I should save the money for uni for my kids to attend Tony Robbins or other mgmt trainings instead of "factory schooling"...

Comments: I would like to congratulate Born To Reign as I am sure yours is a much better way. If I may add (sounds silly as I am still single), do not follow the new mantra to treat your kids as friends. Kids need you to be their parents, not their friends. They have friends of their own. Having said that, parents should also structure their relationship to encourage open sharing, respect for each others' privacy (it applies both ways), respect for each others' opinions, and to establish trust both ways. There must be sufficient trust in that they will tell you when they have made mistakes, hence do not exert excessive punishment on the hint of any missteps as that will make they shy away from telling and sharing future problems and mistakes in their life. There must be a strong vacuum of trust within your family which can only be built by lifelong examples and exemplary ways, values and attitudes.

PS2, the Wii... I see kids ALL THE TIME at dinner tables playing with them. There must be rules and priority. There must be a willingness to spend time talking and sharing. Many parents who work may be tired or prefer to zone out in front of the TV when they are home. Buying them toys or giving them pets are not replacement. Kids are most influenced when they are young. Time lost during those days will be lost forever. How they turn out, if parents fail to exert the right influence, will be based on the roll of the dice then.

Nobody needs a license to be parents. You need a license to drive, to operate heavy equipment, to fly a plane, to be a teacher, to be a professional, you need a degree for most professions... it seems the only thing you do not need a license for is to be a parent. It is not an inborn quality as many parents are idiots as parents. Many kids are but a reflection of their parent's upbringing, and its a vicious cycle. Seems like we need a licensing body for parenting as I am sure most would agree it is the most important job in the world should you decide to take it up.

A few months back, just before the markets collapsed, Microsoft had a $32 per share buyout offer for Yahoo!. Jerry Yang did his yin and yang dance, at the same time talking to Google about a possible tie up which would have made the sale to Microsoft unnecessary. Well, the markets collapsed, Google said adios, Jerry was left to pick up the pieces. Yahoo! shares collapsed to below $10 at one stage before recovering to be just above $12 currently.

Jerry had to step down as CEO for his stubbornness. They are still looking for a new CEO. Into the fray, many big investors and hedge funds took huge positions leading up to Microsoft's bid at $32. Carl Icahn even got onto Yahoo!'s board, and is now left holding a lot of Yahoo! shares in the mid-20s. Carl was pretty pissed at Jerry for delaying the deal with Microsoft.

Microsoft did try to talk about a lesser deal to buy Yahoo!'s search business, but Jerry was right to refuse that also as the search business is pretty critical to Yahoo!'s value as a company.

Google scrapped the deal with Yahoo! which was a revenue sharing deal which would have brought in hundreds of millions for Yahoo!. The deal probably would never have taken off as it is very likely to be thrown out by the Department of Justice on antitrust issues. Basically anything Google touches on internet business now would be scrutinized closely by the DOJ.

Why The Deal Will Be Done

Yahoo! cannot survive on its own for too long. Its revenue and profits will flatten out soon, thus reducing the value of the company - that being the case, it would be better to be absorbed by a bigger company that offer synergies to build on the Yahoo! platform.

DOJ most probably will reject a deal between Yahoo! and Google, but should approve a deal between Microsoft and Yahoo!.

Carl Icahn joined the Yahoo! board in August 2008, holding just under 5% shares of Yahoo!. Following the share price collapse, Carl has bought another 6.78m shares in the first week of December, bringing his stake to 5.45%.

The company is also now exploring a deal to buy or merge with Time Warner's AOL. The thing is Yahoo! cannot and should no longer exist as it is now. Following the collapse in October and November, many hdge funds have had to dump Yahoo! shares bought in the mid-20s thus creating a lot of free float.

There has been talks that Jonathan miller, the ex-CEO of AOL has been trying to assemble a few private equity and sovereign wealth funds to raise $28bn-$30bn to buy Yahoo! That works out to be between $20-$22 per Yahoo! shares. The involvement of Jonathan Miller and or AOL will put a lot of pressure on Microsoft to act soon.

Microsoft was willing to pay $44.6bn a few months back for Yahoo!, I am sure they will pay $25bn now. Microsoft NEEDS Yahoo!.So what is Microsoft waiting for? I think Ballmer is waiting for Yahoo!'s new CEO to be installed. To make a bid now with no inkling on who is running the show would make "synergy and strategy" planning obsolete.

Yahoo! has a strong brand name, a very valuable advertising and search platform, a lot of cash on its books and almost zero debt. Yahoo!'s book value is $8.36 per share.

Google made operating profits of $1.7bn last quarter on revenues of $5.5bn. Yahoo! made $70m last quarter and surprisingly AOL made $268m in the last quarter.

Microsoft needs Yahoo! because Microsoft's online revenues last quarter was $770m but registered an operating loss for THAT quarter amounting to $480m. Microsoft has dumped a lot of money for online businesses and have been failing dismally to get a foothold. It needs Yahoo!'s platform to build on its search and advertising business on the net. The biggest threat to Steve Ballmer would be IF Yahoo! falls into the hands of someone else. Even if Yahoo! is over priced or a mistake or both, its a mistake Microsoft has to make. They cannot keep losing ground to Google and just watch the trains go by.

Concluding comments: If everything is so conclusive why isn't there a bid already. The markets have basically just collapsed over the last 3 months. Credit markets have stopped functioning regularly for a while. Predators trying to raise funds to mount a bid are finding it very difficult to raise $20bn in current markets.

Microsoft knows that it does not need to raise anything to mount a bid. I am sure they will try to come up with deal that would be much lower than the $32 per share. I am also sure they would instantly be involved in a bidding war if someone else started the bidding. Under normal markets, many arbs traders would have taken positions in Yahoo!, maybe even up to $16 in anticipation of a $20-$24 buyout offer. But under current market conditions, capital for arbs may have shrunk and the many hedge funds are now tackling redemption worries rather than looking actively at potential buyout special situations.

WSJ: The International Monetary Fund's top economist generally endorsed the incoming Obama administration's approach to economic stimulus, and urged countries to consider offering a kind of "recession insurance."

President-elect Barack Obama's economic team is weighing a stimulus plan that would cost somewhere between $675 billion and $775 billion over two years, and would be used largely for construction and other government spending. The package is likely to include a temporary tax cut of as much as $1,000 for middle-income families.

Olivier Blanchard, the IMF's chief economist, said "the size corresponds roughly to what we think is needed." He backed the Obama approach of targeted tax cuts, saying the money should go to consumers who are "truly credit constrained."

In an accompanying research paper, Mr. Blanchard and three other IMF economists advised against broad cuts in corporate tax rates, dividends and capital gains -- Republican favorites -- which they judge "likely to be ineffective" because profits are low. The changes "are often difficult to reverse," they added.

In an interview, Mr. Blanchard said a general tax cut may be less effective than other measures because many consumers would save the money.

IMF recommendations rarely have much clout in the U.S., but the timing of the paper and Mr. Blanchard's comments may make a difference, as the Obama team is looking to present its plans as responsible and widely acceptable.

The findings pose another hurdle for Republicans. Former Bush White House economist Glenn Hubbard argues that despite the IMF findings, a broad corporate tax cut would spur investment and boost stock prices.

Mr. Blanchard, on leave from the Massachusetts Institute of Technology, has long done research with Mr. Obama's chief economic adviser, Lawrence Summers. A spokeswoman for the Obama transition office didn't comment on the IMF findings, but said "economists across the ideological spectrum agree that the danger is doing too little to get our economy moving again, not too much."

The IMF has long urged China to take similar steps to boost its economy. Overall, the IMF has been campaigning for a global stimulus plan of 2% of world gross domestic product -- or more than $1 trillion.

Not all the IMF's comments supported Mr. Obama. Mr. Blanchard warned plans to bail out car companies could prompt a trade fight if other nations tried to match U.S. aid. He said countries should focus on providing credit in the case of corporate restructurings.

Among the IMF's proposals is a kind of "recession insurance." Under that plan, individual governments would offer insurance to firms and individuals that would pay off if GDP sank below a certain level.

"Widespread use of such [recession insurance] contracts would provide an additional automatic stabilizer because payments would be made when they are most needed, namely in bad times," the IMF paper said.

With such instruments, Mr. Blanchard acknowledged, potential buyers might worry whether, during a downturn, governments would make the payouts.

Based on the global market prognosis written over the last few days, I have compiled stocks which will stand to benefit (should they pan out they way I anticipate). Again, these are not stock recommendations, these are my own shopping list - not a call for readers to buy. Consult your own investment advisers before making any investment decisions.

INTERNATIONAL STOCKS

DryShips Inc. (DRYS) Current price $9.69 52 week High-Low: $116.43-$3.04

Petrochina-H (0857.HK) Current Price HKD6.36 52 week High-Low: HKD12.40-HKD4.05

Toyota ( 7203.JT) Current price 2,900 yen 52 week High-Low: 6,400 yen - 2,585 yen

China Mobile (941:HK) Current price HKD74.50 52 week High-Low: HKD138.98 - HKD58.50

* this is a high risk portfolio which one should not commit more than 10% of their investible funds, it is also likely that the exercise price will not be reached within the time to expiry, its an aggressive trade whereby one may make 100%-300% based on the anticipated recovery before March 2009

The prognosis was an unhedged opinion. After criticising economists and analysts for being wishy-washy, ... "on the one hand, however if the other thing happens..." , so i am glad some readers realised it was a straight out opinion. I do not expect many to agree, so thanks for the feedback. Its much easier to continue to be bearish, just regurgitate whats in the media - but of course I could be wrong. I will try to clarify some of the concerns, not to sway you, but to explain further my views.

Toxic assets too huge - It seems too big because its a one way traffic. It seems too big because of the unwinding and de-leveraging trends. It seems too big because everybody wants to be first out best dressed. What we have to be aware is that sometime soon these cash and liquidity will have to be placed out in some form or other. It seems too big because of risk aversion, rather than the inability to deal with the issues.

It will take a much longer time - Let's get the facts. Even during the Great Depression, we saw recessions lasting 22 months, and to me, its largely because we did not have the fiscal or monetary knowledge or tools to deal effectively and immediately with the issues then. In other views, some will argue that Japan too more than 10 years to work itself out of its 90s credit bubble. Well, thats because Japan did nothing for the first 10 years, seriously folks. If you compare to the immediacy of the many moves to tackle the issues during the current crisis, we would have a better appreciation of the comparison.

There are still time bombs - The greatest thing about this American financial markets, is their transparency. When the proverbial stuff hits the fan, everybody will be clamoring to rip open all wounds, especially the affected firms. The affected firms had to lay it all down as its pointless to try to hide. In fact, it would be a very shrewd move to let it all out so as to be part of the bailout. The transparency thing is very good because their firms are so large, i.e. no one main owner operated financial behemoth. Usually the largest shareholder holds less than 10%. The scrutiny is magnified with independent directors trying to save their behinds, not to mention the vulture bond holders trying to see if the firm is worth anything at all.

Is Roubini wrong then? - You all know I think the world of Nouriel Roubini. I have highlighted many of his opinions and he is by far the most astute and correct economist on the current financial turmoil bar none. By his accounts, he still sees some pockets of danger in the economy, but he is not as bearish now as he was a few months back. We also should note that a number of things are very fluid - Roubini worked with Timothy Geithner and Lawrence Summers many years in recent years. You can bet that the 3 of them will be discussing intimately on ways to address the issues. You cannot get better advice than from the man who predicted the carnage step by step, can you?

The new team - Well you have Geithner, Summers and de facto Roubini, throw in Paul Volcker as well - is that a more credible team than Paulson and Bernanke? The team has been planning the actual fiscal stimulus and various remedies for the issues at hand. What started out as a $350bn plan has morphed to $600bn and now is likely to top $1 trillion. They are not shy about it, and they want to stamp their mark the moment Obama takes office come mid January. On actual economics data, each $1bn spent on infrastructure will create 35,000 jobs. The team is also wary that the stimulus will not go overseas immediately to create jobs outside of the US, hence expect more on healthcare, education and infrastructure spending.

Too giddy on Obama - Some may be questioning that I have gone overboard on the optimism riding on the Obama factor. But I have been following articles and interviews on him and how he has been picking his team members. The more I read, the more convinced I am that we have the best person to lead, he is also an astute and well prepared manager. He is, in a single word, competent. If you look at how he organised his campaign for the elections, it was a focused and effective. Above the fray, above the meanness, focused on the issues and getting to the heart of the matter. Oratory skills aside, he exhibited high intelligence, a general amount of ego and deserved self-confidence. The so called goodwill riding on him when he takes office should not be discounted - anyways what better way to deal with esoteric problems such as risk aversion and irrational fear than to match it with unmitigated goodwill laced with competence.

What about demand destruction - Exports are down, shipping rates have plunged, oil price is nearing $30... surely there must be demand destruction! Or is there? There is a fundamental price for everything based on demand and supply. The irrational peaks in commodity prices has more to do with liquidity surplus, the rise of commodity centered funds, the rise of hedge funds playing trend and momentum investing, the unquestioning acceptance of analysts far fetched supply inadequacies years ahead of us... Read the EIA's weekly US oil import data. In the week ending Dec. 19, total US oil imports were 12.780M/day, versus 12.907M/day in the same week a year ago. That's only a 1.0% drop - where is hell is the demand destruction? The global credit crunch resulted in forced liquidation of global supply chains, as every one liquidated their inventory to raise cash in order to survive. The inventory sales flood the market to create a false over-supply situation while supply destruction is playing out at break-neck pace as unprofitable mines are shut down. That tells me that for many resources, we are forced to work down a lot of inventory rather than seeing a genuine demand destruction. Commodity prices were artificially high 6 months back, now its the other extreme. Very soon, we will see shipping rates on the upswing again as not only is inventory very low, but many have mistakenly shut down mines and harvesting as well.

p/s photo: Anna Tsuchiya

pps: Over the next few days I will blog on the recommended international stocks, local stocks and a high-risk portfolio selections, all based on my global market prognosis. Its been more than 6 months since I have made stocks recommendations.

Prognosis: the prospect of recovery as anticipated from the usual course of disease or peculiarities of the case

Overview – This strategy piece will probably be regarded as the more optimistic one you will ever come across in these turbulent times. I am quietly (or not so quietly) optimistic for 2009 and beyond for global stock markets. I believe we have seen the groundwork laid for possibly the mother of all bull markets over the next 3 years. It should be a gradual stop-start thing. It will be one which is loaded with inflationary pressures as well.

Expectations – The trouble with many investors is that we are always only able to perceive and view things within a certain perimeter. Back in January 2008, there were still many who viewed the global economy with a sense of bullishness, and that the real issue was higher commodity prices. We tend to feel and sense things happening around us at that point in time. Now we are surrounded by layoffs, that the many injections of liquidity are unstoppable, that the many rate cuts are insufficient, that the mother of all fiscal measures may not be adequate, that lending and risk aversion are still kings of the world – it is natural then to assume that we have a long way to go. As we sit in the middle of this crisis, it is also natural to hear experts proclaim that this is the deepest recessions the world has seen since the Depression. It is logical to conclude that we are in for the long haul. We let things around us shape the bulk of our investing decisions, when we should base our investing decisions on what things will be like 6-12 months down the road. Just like back in January 2008, we should base our investing decisions on things happening 6-12 months down the road, and not how things were like at that point in time.

The Recession – As announced a few weeks back, the recession started in November 2007, and as we stand now, its 14 months deep in recession. Prior to World War II recessions were more prolonged and deep, usually 18-22 months. Mostly it’s that the tools available to governments and central banks to deal with recessions and their effects were very limited then. The understanding of monetary and fiscal stimulus were in its infancy then. Post WW II till today, the longest recessions by ranking were:

November 1973 – March 1975:16 months

July 1981 – November 1982:16 months

December 1969 – November 1970:11 months

April 1960 – February 1961:10 months

The average being 11 months, and this present recession is already past the average at 14 months. Of course we cannot be satisfied just knowing it is already past the median. We cannot just imply that things are towards the end just based on averages, we are not in a baseball game.

Its Different this Time – This idea that things are different this time around will cost you your life savings. The more things evolve, the more things stay the same. This recessions’ fundamentals deterioration may be more widespread, but so are the measures doled out to rectify the patient. Its not really different, it just seems that way when you are in the midst of it. Business cycles are called cycles for many reasons. Things will peak and they will drop, they will boom and they will bust, each boom and bust will have their own stories to tell, but the cycle remains the same. The gravity of this crisis is matched by the unprecedented cooperation by all nations to work as one to rectify the problem. The amount of additional fiscal stimulus and the coordinated rate cuts are unprecedented. On November 9, China announced a $586B domestic stimulus package, more than triple the size of America's 2008 package. Australia announced a $10.4B package and Japan a $51B. Lump in the recent moves by EU, and the likelihood of a major one by Obama when he takes office, and you have a sense of its magnitude.

Owing to the high risk to aversion now, I believe the fiscal measures undertaken so far may have gone past what is required to bring back liquidity and consumer demand to the forefront. When your anorexic fishes are not eating, you might tend to throw everything at it to get them to eat - its actually more than they can consume even for a healthy fish. Once they start to eat again, they will find that there is actually too much food in the fridge.

You try to bake a nice cake, you have put in all the right ingredients into the bowl. Its enough to be a mother of all cakes... but no one is stirring the pot... yet. For pot stirrer information, please read on.

Confidence – The risk aversion mentality has taken strong roots, thus delaying the effects of the many measures being instituted. In fact, it is likely that we have already over-injected the required sums to revive many problem areas. It’s the confidence in the system that is wreaking havoc still. Confidence and risk aversion can also become a bubble condition – just look at the rush into yen and the rush into USD and US Treasuries. If those are not at bubble levels, I don’t know what it. Just like a pendulum, things will always sway to extremes before righting itself. I am not saying that the credit situation is over. I still think there are pockets of danger in credit cards.

Why Mother of All Bull Markets – We are seeing a readiness to go to zero interest rates in most major economies’ monetary policies. In a normal market situation, the rapid rate cuts will be balanced with a re-rating of stocks and yields, but they have not had that effect because the risk aversion mentality still rules. But that is OK, it just delays the “bull” not that the bull is not around. The bull will always surface when the right factors congregate.

The global economy has grown by nearly 70% in size from 2007 till mid 2008 before things imploded. Things imploded because of derivatives and capital issues. Yes those liquidity or multiplied liquidity was drained from the system, but it would be silly to think that they were responsible for the bulk of the 70% growth in global trade. What we have seen over the last 8 years was a huge rise in global middle class, in particular from the BRIC nations. This huge new middle class will still be consuming more resources as more emerging economies continue to pour resources to build up infrastructure. That is the inevitable “good” that comes from globalization. The demand on our resources was highlighted over the last 3 years when commodity prices went through the roof. Their price rises may have been exaggerated by the remarkable liquidity from hedge funds and specialized funds – but the underlying principle still remains. The implosion in commodity prices over the last 6 months was more due to the retraction of liquidity, rather than a rapid deterioration in demand fundamentals.

The secular bull in commodities was caused by perceptions of massive demand in emerging markets, particularly the BRIC nations - Brazil, Russia, India, and China - which were growing at unprecedented rates. As they became increasingly wealthy and industrialized, these economies represented growing new demand for energy, food and production inputs. The commodity price collapse since the summer of 2008 does not indicate inflation is out of the question - it indicates global economies are contracting deeply. The amount of new fiscal measures by the said nations will go some way to addressing the contraction slide. Mind you, all this while, we still have this new huge middle class in the global economy.

Inventory & Capacity Utilisation - Most companies have already worked down their inventory levels over the past 6 months in anticipation of weaker demand. Resource companies have shut down certain plants to reduce production capacity. All told, the current situation sees a very level of inventory for essential goods. Companies have been quicker to respond to market changes or better at trying to anticipate market trends. The scenario also pans out well for a confluence of factors to rebound smartly on the slightest hint of recovery. For example, palm oil exports have been haunted by buyers reneging and sharp drops in demand. Users have been working down on their inventory. Yesterday, data showed that exports for the December 1-25 period soared 24 per cent to 1,345,325 million tonnes from 1,087,865 tonnes shipped in the same period last month.

Inflation – Following on the above premise, it is safe to say that inflation will rise when confidence returns. Central banks will then have to drain liquidity from the system gradually. As the risk aversion was so strong, it is likely that most central banks will allow the markets to rise, and even allow inflation to seep in for the first 12 months. You do not want to ruin the hard work by tightening the noose so soon. Hence the first 12 months will be most vibrant and exciting.

Darkest Before Dawn - Investors were bailing out of mutual funds at record pace, the VIX set new highs, more than 90% of closed-end funds were trading at a discount that were much higher than the average. All these are signs of bottoming. As I have written before, it should be very useful to look for bottoms by looking at the yen/usd rate. You need risk aversion to reduce before investors are willing to get back into stocks.

Cheap valuations are a reflection of risk aversion, the rush to US Treasuries is a sure sign of risk aversion, the rush to USD and yen are a sign of definite risk aversion.

Gem #1: Markets will only start a genuine recovery when risk aversion subsides

Gem#2: Risk aversion reduction will be immediately reflected in weaker USD and yen

The fall in USD over the last two days is more due to the zero interest rate regime enacted by Federal Reserve, so that should not be a sign of risk aversion reduction.

The best guide for locating current markets' bottom: WHEN USD and YEN BOTH STARTS TO FALL IN VALUE in a sustained pattern.When these two currencies fall, it show a willingness to move exposure into other currencies or assets, be it stock or bonds. Before they are reflected in the prices, the signal will be most apparent in the currencies.

However, even then we cannot really ascertain a buying trigger. So, my advice would be to break up you investing funds into 3 portions, get ready your list of stocks to buy.

Catalyst #1: When yen/usd rate moves back to 94, plonk down 1/3 of your funds

Catalyst #2: When the rate moves to 97, move the second portion

Catalyst #3: When the rate breaks 100, move the rest in

A point not missed here is that if yen weakens against the USD, the latter would be gaining in strength. However, I am using the yen/usd rate as a guide, as I believe when the yen starts to weaken, the USD would also weaken, but not by as much - i.e. the USD would gain ground against yen but at the same time lose ground against the euros and other major currencies. I use the yen/usd rate because that is most widely followed. The yen is used as the determinant because it was the most popular currency for carry trades, the unbelievable strength now is due to risk aversion as the Japanese exporters are basically losing money and cannot compete below 90.

Comforting Data – Over the past 50 years, the S&P 500 tends to bottom:

One quarter before the GDP bottoms; 3 months before the ISM manufacturing survey bottoms; 7 months before the peak unemployment rate; 4 months before the largest decline in non-farm payrolls; and4 months before the bottom in consumer confidence surveys.

Using that as benchmarks,we should expect a genuine economic recovery somewhere between March and June of 2009.

The Obama Factor – Just like investing, to move share prices you need catalysts to make things happen. Risk aversion does not just go away, they also need to have catalysts. Obama will take office in January 2009. Call it goodwill, call it anything you want. He has already assembled a group of very credible people to help him. He has shown a clarity and purpose in hiring the best, rather than just from his own circles. The key would be the stimulus package he will be announcing. What started off as a $350bn package has now ballooned to $600bn, and now its likely to top $1 trillion.

Its not just a hopeful thing. As mentioned, the groundwork has been laid: very low interest rates, very high risk aversion, stocks at very cheap levels, governments pumping fiscal stimulus like crazy… its like everyone is working towards an Obama effect.

Confidence is a strange yet important part of global finance. A basic re-rating of 10% jump from current levels will improve valuations for a lot of toxic assets as well and in turn relives the constant need to raise capital. Further jumps in markets will see a willingness to buy even toxic assets. Things that look like being worth just 20 cents to the dollar may now be worth 50 cents to the dollar. It’s a cumulative snowball effect. Injured banks may even be able to use the capital raise to actually repair balance sheet and do actual lending, instead of constantly having to write down every quarter. You would be amazed what a 10%-20% jump in equity prices can do to the entire system.

I am looking for the Dow to reach 10,000 by February / March 2009 and to go back to 12,000 by June 2009. I cannot safely say what will happen for the second half of 2009. A lot will depend on what the central banks and governments do over the next 6 months. If they play their cards right, I think global equity markets could fully recover by end 2009 and go on a 2-3 year unprecedented bull run.

Readers of this blog will know that I have been pretty bearish on Malaysian properties, but even more so for Singapore and HK properties. The latter two have seen a 10%-15% price correction across the board. The funny thing is that Malaysian property is holding up pretty well.

Over the last few days a couple of things struck me about Malaysian properties, which have eluded me, and many property analysts. We always look at the same indicators: affordability ratios, employment trends, rental vacancies, occupancy rates, ratio of income to mortgage, etc.

Somehow there are a couple more reasons which seem to dictate the underlying strength of local property prices.

a) Open economy - The more open your economy is to free trade, the more susceptible you are to global financial turmoil. Hence explaining much of the distress in HK and Singapore economies. Theoretically speaking Malaysia should be affected just as bad, but we are not. I would like to cite this as the Shenzhen effect. Malaysia has what I would coin as the "Shenzhen effect". Its when a place can be used to produce goods and services more cost effectively. We also must remember that we are in a massive globalisation mode for the past 15 years, with the pace rising over the last 5 years. There is no way you can bring back those jobs to Singapore, HK or the US unless maybe if the Sing dollar goes to 1.5 vs the ringgit or the HKD drops to 15 HK dollar to the USD.

The key point is that when global companies decide where to cut cost or restructure, they now tend to leave Malaysia alone. You cannot cut manufacturing outright, you reduce shifts and capacity. But you can cut services and managerial headcount easily and the numbers make more sense out of places such as Singapore and HK.I give you another example, in investment banking, a senior analyst may be paid a US$300,000 package in South Korea or HK, but a similar position in the same firm in Malaysia may be paying just US$120,000. Its not all equal. And when top managers strategise on where to lop off manufacturing and investments, Malaysia will almost be the last to be chop.

Why? Multi lingual work force, relatively hard working staff (I said relatively), very cheap land cost, very cheap building and facility cost, excellent ports and road networks to ship in and out, reliable and effective air travel hubs in the country, much safer and stable politically, less risk of war or internal unrest, high degree of safety from terrorism, its Islamic yet Islamic neutral for businesses which is a highly coveted position to all, strategically, its position is important for shipping services.

b) Many have over invested in India and China, hence some operations investing may be delayed or see its capacity being shrunk there. HK and Singapore are the high value add sectors and are also highly leveraged to global financial markets, they cannot hide. Hence we cannot and should not lump Malaysia together with HK and Singapore. yes we will see some jobs lost but it should not be anywhere near the cuts we are seeing in HK and Singapore.

We always just talk about speculation in markets, but we should also look at sectors or countries that have over invested (either from domestic or foreign sources). Singapore has over invested in private bankers, same with HK. Singapore has over invested in Sentosa and the outlying real estate areas where prices are totally out of whack - we are seeing Monaco prices and the weather is too damn hot! China has many areas that have seen over investment as well.

In terms of speculation, Singapore is topping the charts with the en bloc sale, which proceeds are then geared up to speculate in the many luxury condos. Enough said. Specuation is there in Malaysian properties, in particular the high end condos - we have never been able to maintain very high prices in condos because most people still prefer houses and land. The only time we see RM1,500-3,000psf is in a bubble. The correction will be most severe in those above RM1,000psf which may see a 15%-20% drop. The RM500-999 psf may see a drop half of that. Landed properties below RM1.5m are still pretty solid and may only see a 5% drop from their peaks. Those under RM3m may see a slight ease off but it should not be major. Higher than RM3m, they are in a world of their own.

c) The stock market effect - If you were to look at the financial turmoil in the past, namely, the mid-late 80s, the blip in 1994, the major monster of 97, the internet bust, the SARS effect, the tsunami effect and now the credit implosion... you can chart a very useful multiplier effect from losses in the stock markets. Prior to 2000, any kind of financial bust ups will see a lot of havoc and bad debts, ask any remisier... Following moves to limit contra and contango trades, this has removed a HUGE "leveraged disaster" from the domestic economy.

I can give you the excellent example of my 6 analysts working with me in mid 90s, their monthly salaries between RM3,000-10,000 and basically under 30 and real net worth probably zero. But each and everyone of them will have zero deposit with 2 or 3 remisiers, but personally will have a contra position of between RM100,000-300,000 in a few stocks depending on the mood of the market. This is not unique to my team of people, everybody everywhere were doing it. Naturally we always see a huge multiplier effect when the market corrects 10% over a week.

Since 2000 any major financial calamity has not seen similar catastrophic personal financial aftermaths.Now you try to buy RM50,000 worth of share with zero deposit, your remisier will ask you to fly wau. This market correction was also unique to the majority of retail stock players. Many were able to sell down most of their stocks or just stop playing stocks when the market retreated from 1,400 to 1,200... sure some will still hold a few stocks in their portfolio but many have been able to avoid the carnage. When a market falls from 1,400 to 850 its the holders of the shares that bear the brunt.

This time around retail players have been able to sidestep much of the disaster movie, its the funds that got whacked royally this time, ... local, hedge and foreign.Thus this will further help explain why most Malaysians are still relatively cash rich and under invested. Fewer job losses and fewer after effects from the stock markets = less likelihood to need to sell properties in desperation.

I am working on a big piece on the Market Prognosis for 2009, stay tuned, will be out in a couple of days.

This post may come off as a bit unusual but its my Christmas gift to all...

The Western world is full of hugs and kisses, so much so that at times they lose their meaning. The Eastern traditional world is usually the opposite, families and good friends find it enormously difficult to say "I love you" or even give a pat on the shoulder, don't even mention a hug.

In Asia, we find it hard to say affectionate words or even give our parents, loved ones or relatives a simple hug. Words are inventive and can just roll off our tongue, repeatedly saying them is good but sometimes they just lose their effect and essence. Even the usual kisses or pecks become a bit perfunctory.

This Christmas, let the people you love know, really know how much you love them, leaving nothing on the table. Here's how to do it:When you see your loved ones, go to them and slowly stretch out your arms. Ignore whatever they may be saying to you: "what are you doing", "whats up"...etc..

Then just hug them, no words, close your eyes and just think how much you love them despite our many failings and weaknesses as friends, as lovers, as parents, as relatives. The person being hugged may now say things like: "is there something wrong", "what's up with you", "are you alright"... Do not reply... just continue to hug for at least 20-30 seconds... the rule being "Do not be the first to let go", the second rule "Do not say anything", let the touch and pressure of your hug communicate how you feel.

After the initial suspicion, the person should be able to feel what you are trying to say. When words get in the way, give them a real hug. After 20-30 seconds, just smile and say "I really wanted you to know that I love you, and I am so glad you are part of my life" (or something along those lines...)

Blessed Christmas y'all!

p/s photos: Ueto Aya, Chen Kuang Yi, Zhou Wei Tong, Sarah Malakul Lane

One of the very under-rated talent in TVB is Bondy Chiu Hok Yee. She plays good supporting roles but was never promoted as the lead actress. Her singing career was a stop-start thing, never fully promoted or marketed properly. She had a decent album in 2000, Slower Is Better. She has had a long break after really breaking her leg. Prior to that she did some good stuff in dramatic plays. Somehow the timing and confluence of things look right this time around. The new album was released on 10th December called "`ting". Its pretty exceptional. I have included 3 of her older songs on the imeen jukebox for sampling pleasure. Try and get this album before she becomes really successful.

Yesasia Editorial Description Of Album: Having changed her focus to acting with appearances in television shows and stage productions, singer Bondy Chiu has been absent from the Canto-pop scene in recent years. But now she's back with her most important project yet, a self-financed, independently produced album titled "Listen", her first non-compilation CD since INSIDE in 1999. Here, she covers 11 beloved Chinese pop songs with refreshing jazz arrangements, including "My Love Goodnight", originally sung by Sally Yeh (Track 2), "If It's Love" by Leon Lai (Track 9), "Kiss Goodbye" by Jacky Cheung (Track 10), and "Wish You Well" by Chilam Cheung (Track 11). Made with true music fans and audiophiles in mind, Bondy's album was recorded with a band of brilliant local musicians using high-standard instruments, and the limited first press version, manufactured in the UK, will be especially sought after.

動心演繹 聆的突破

.本地最強樂手演奏 .真空管咪高峰錄音 .丁級混音器材製版 .首批限量英國壓碟

01. 我可以抱你嗎 02. 長夜 My Love Goodnight 03. Be Your Love 04. 情深緣淺 05. 曾在你懷抱 06. 許願樹 07. 對一個人愛錯 08. 某月某夜 09. 如果這是情 10. 吻別 11. 祝君好

I believe this is her best move, Bondy being Bondy, will not find those commercial big backers. Hence she will not get good songwriters to write songs for her. I think her selection of doing popular songs over the last 20 years will showcase her voice well. Most of the songs has been reworked with a jazzy feel ala 2V1G. If you cannot find it in shops, you should try to get it on the net:

Related Party Transactions - A business deal or arrangement between two parties who are joined by a special relationship prior to the deal. For example, a business transaction between a major shareholder and the corporation would be deemed a related-party transaction.

While the great majority of related-party transactions are perfectly normal, the special relationship inherent between the involved parties creates potential conflicts of interest which can result in actions which benefit the people involved as opposed to the shareholders. Parties are related if one has control, or joint control, or significant influence over the other [IAS24R.9]. Significant influence is relevant when it relates to financial or operating decisions. Parties are also related when they are under the common control of another entity. The existence of control, joint control or influence can affect the terms on which the two parties transact. An understanding of the relationship and the terms on which two related parties have transacted is therefore relevant in understanding an entity's financial statements.

Why RPT deserves very close attention:

a) potential for collusion

b) minority interests are ignored or diminished or decimated

c) cashing out at the expense of one related party, which comes at the expense of the minority shareholders of the affected company

d) RPT generally devalues the perceived integrity of a company, collectively they devalue the integrity of the stock market

I am certain that the Securities Commission has a mandate to closely monitor RPTs. However, corporate owners will always try to circumvent rules or push through RPTs. Lately, in light of the current global financial turmoil, we have seen a rise in questionable RPTs. Some are deliberately designed to bypass the Securities Commission. When they are designed that way, it should be more questionable. I hope the SC and Bursa can still impose "discretionary powers" to regulate these RPTs.

Example #1: MMC-Senai Airport deal

This was supposed to be an all shares deal, which would have had to be approved by SC. They changed it to an all cash deal which only requires the approval of shareholders. Syed Mokhtar owns 51.8% of MMC, and as the controlling shareholder will usually abstain from voting. There is nothing that says that some of the minority shareholders may still be linked or connected to the controlling shareholder. The RM1.95bn shares deal was changed to RM1.7bn all cash deal. Though Senai Airport Terminal was valued at RM2.2bn, there are still a lot of questions.Why should MMC buy over the company? The extensive landbank does not gel with MMC's business model. If you really want value, you should consider listing Senai Airport Terminal when the market recovers.

Doing it now looks like somebody needs the cash. MMC is cash rich, is SAT in trouble with cash flow? If it is, then the deal would be detrimental to MMC's minority shareholders. If it is not, SAT would be better off with its own listing with its extensive landbank. If SAT cannot list because it is not profitable, why should MMC even consider buying then?

A prudent board would ask for SAT to go through a public bidding if the said value is RM2.2bn, why no such thing was considered? There shouldn't be an all cash deal for some asset that is still not profitable. An all shares deal would be more advisable.

Example #2: Magnum's asset disposal

Magnum proposed to divest some non-gaming assets to company director Lawrence Lim. Even that first sentence assumes all readers are stupid. The rationale was that Lim would then procure the buyers for the assets and probably make a cut for himself. This silly move again bypasses SC's jurisdiction. Lim is paying only RM3m downpayment for the assets worth RM130m - you go to a bank to buy a house also requires a minimum of 10% deposit, what is this crap? If he cannot get a buyer at a higher price than RM130m, he basically loses just RM3m. What a good betting opportunity. I mean at least IOI lost a huge bundle when it decided not to buy Menara Citibank, at least thats fair.

As a company director, shouldn't it be prudent to engage an investment bank to dispose off these assets?

It is so hard to write without profanities when describing these RPTs. I hope the SC will step in with their discretionary powers. When did we revert to a cowboy market?

Michael Lewis wrote possibly the funniest semi-biographical book on Wall Street entitled Liar's Poker. Below was his most recent article:

Dropping out on Wall Street

Michael Lewis

December 19, 2008

Recently I received a letter from a young employee of a well-known financial firm, who asked that I not mention his name, his employer or anything else that might give him away. Though a bit short on self-pity, this letter was otherwise a fine example of a sort I've received often these past few months.

"I am writing you for advice," Anthony (let us call him) began. "I graduated in May of 2008 and since July have spent my time entangled in the culture of (his well-known New York bank). I'm thinking about leaving. My dad laboured his whole life so I could have the opportunity to do something like this, so leaving isn't exactly what I want to do. I know if I stay here I could work unbelievably hard and move through the ranks, or maybe move firms [but] I guess I'm starting to question the whole securities industry."

The young man went on to concede that what attracted him to Wall Street was the chance to get rich quickly, and the excitement - but that both of these things now seem gone forever.

"So I have this plan to go to Hollywood," he wrote, but then instantly undermined himself. "I feel confused, a little stupid, but yet somewhat confident. I mean, I read your book, I figured out how to get to Wall Street from a non-Ivy League school, and I got here. The only question now is, if I leave, where do I go?"

Let me try to help sort it out:

Dear Anthony,

On several occasions I have taken my own advice and it has almost killed me, and so I'm a tad uneasy about offering it up to you. But if you promise not to take it any more seriously than I do, I'll answer you as best I can.

Let's start by putting your problem into perspective: you still have a job. You work at one of the world's biggest banks. It's true, the thrill and money is rapidly being drained from such places. Your big bank, like all the other big banks, seems to be in the process of being nationalised - thus the longer you stay the more you may find yourself in something resembling a government job.

But that's not all bad: government jobs are secure. You are also young, in your early 20s, and without a family to support. That is, unlike the vast majority of the people on and off Wall Street, you have the luxury to wallow in your misfortune.

Now let's wallow. We're at the beginning of a recalibration of the role of finance in global economic life. The excitement and the money that attracted you to Wall Street will probably not return for a long time. If these really are the only reasons you became a financier you probably should find something else to do with your life.

But before you go lurching into Hollywood, let us make sure you aren't simply repeating the mistake you made by lurching onto Wall Street. That is, let us focus less on your immediate condition - safely employed but disillusioned - to the habits and beliefs that led you into it.

You were never exactly wrong. If you'd been born 10 years earlier and behaved exactly as you have done, your career might well have made you as rich and seemingly successful as you imagined your father wanted you to be. You simply came to Wall Street too late, and are in the strange position of a man who won the lottery on the first day there was nothing in the pot. The mistake you made, in your view, is to have played the lottery on the wrong day. The mistake you made, in mine, was to have played the lottery at all.

There's a question you might ask yourself: Am I looking for a job, or a calling? On the one hand, the importance you attach to your career suggests a desire for a calling; on the other, your instinct to abandon your chosen career the moment it ceases to offer an easy path to fame and fortune suggests that what you're really in the market for is a job.

The distinction is artificial but worth drawing. A job will never satisfy you all by itself, but it will afford you security and the chance to pursue an exciting and fulfilling life outside of your work. A calling is an activity you find so compelling that you wind up organising your entire self around it, often to the detriment of your life outside of it.

There's no shame in either. Each has costs and benefits. There is no reason to make a fetish of your career. There are activities other than work in which to find meaning and pleasure and even a sense of self-importance - you just need to learn how to look.

Reading between the lines, I sense that some of your anxiety is caused by your desire for the benefits of each - job and calling - without the costs. Perhaps that is what led you to Wall Street, and why your mind now turns to Hollywood.

What Wall Street did so well, for so long, was to give people jobs that they could pass off to themselves and others as callings. Such was their exalted social and financial status: Wall Street jobs made people feel special without actually having to be special. You never really had to explain why you were doing it - even if you should have.

But really, the same rule that applies to properly functioning financial markets applies to other markets: There's a direct relationship between risk and reward. A fantastically rewarding career usually requires you to take fantastic risks. To get your seat at the table on Wall Street you may have passed through a fine filter, but you took no real risk. You were just being paid, briefly, as if you had.

So which is it: job or calling? You can answer the question directly, or allow time to answer it for you. Either way, I think you'd be happier if you stopped thinking of what the world had to offer you, and started thinking a bit more about what you had to offer the world. Real excitement isn't just in whatever you happen to be doing, but in what you bring to it. In the end, you have to look for it not on the outside, but on the inside.

Bloomberg

Michael Lewis is the author of Liar's Poker, Moneyball and The Blind Side.